Accounting

- 2021 Federal Fall Economic Statement

- New Compilation Engagement Report

- Ontario’s Not-for-Profit Corporations Act, 2010

- Proposed New Trust Reporting information requirements

- Regional Opportunity Investment Tax Credit (ROITC)

- Common Questions on the Principal Residence Exemption

Human Resources Solutions

Wealth Management

Firm News

- Introducing Ward & Uptigrove Transactional Services

- Donations to Help Offset Negative Impact of COVID-19

- Carbon Footprint Initiative

- Staff Updates

Please Note Our Christmas Shutdown

The offices of Ward & Uptigrove will be closed from 3:00 pm on Friday, December 24th and reopening in the New Year on Monday, January 3rd.

2021 Federal Fall Economic Statement

On December 14, 2021, the 2021 federal fall economic statement was presented. No changes were announced to personal or corporate income tax rates, but the economic statement did announce the following measures:

- Introduce a 25% refundable tax credit for small businesses that incur expenses for air quality improvements in qualifying locations between September 1, 2021 and December 31, 2022

- Enhance the home office expense deduction

- Enhance the eligible educator school supply tax credit for teachers

Small Businesses Air Quality Improvement Tax Credit (“SMAQITC”)

To encourage small businesses to invest in better ventilation and air filtration to improve indoor air quality, the Government proposes to introduce a temporary SMAQITC. The tax credit would be available to eligible entities in respect of qualifying expenditures attributable to air quality improvements in qualifying locations incurred between September 1, 2021 and December 31, 2022.

The tax credit would be refundable and have a credit rate of 25% that would apply to an eligible entity’s qualification expenditures. An eligible entity would be limited to a maximum of $10,000 in qualifying expenditures per qualifying location and a maximum of $50,000 across all qualifying locations. The limits on qualifying expenditures would need to be shared among affiliated businesses.

Qualifying expenditures would include expenses directly attributable to the purchase, installation, upgrade, or conversion of mechanical heating, ventilation and air conditioning (HVAC) systems, as well as the purchase of devices designed to filter air using high efficiency particulate air (HEPA) filters, the primary purpose of which is to increase outdoor air intake or to improve air cleaning or air filtration.

Qualifying locations would include properties used by an eligible entity primarily in the course of its ordinary commercial activities in Canada (including rental activities), excluding self-contained domestic establishments (i.e., a place of residence in which a person generally sleeps or eats).

Home Office Expenses

To continue to support Canadians working from home due to the pandemic, the government will extend the simplified rules for deducting home office expenses and increase the temporary flat rate to $500 annually. These rules will apply to the 2021 and 2022 tax years. For details on the simplified rules introduced in 2020, see our previous article which will be updated as the legislation becomes available.

Enhanced Support for Teachers

The government proposes to expand and enrich the Eligible Educator School Supply Tax Credit to allow teachers and early childhood educators to claim a refundable tax credit worth 25 per cent (up from 15 per cent) of up to $1,000, and to ensure that purchased supplies may be eligible no matter where they are used.

The government also proposes to expand the list of eligible teaching supplies to include electronic devices such as graphing calculators, digital timers, and tools for remote learning. These enhancements would take effect starting with the 2021 tax year.

What We Didn’t See in the Economic Statement

Immediate Expensing Measure from the 2021 Federal Budget

As noted in our July 23, 2021 tax alert, the 2021 federal budget announced immediate expensing of many capital asset purchases with an effective date of April 19, 2021. There is still no draft legislation for this measure and no update was provided in the economic statement.

Given the government’s delay with introducing draft legislation for this measure, our recommendation is to assume this measure won’t be enacted in making capital asset purchase decisions until such time that we see draft legislation being introduced. If draft legislation is introduced and the effective date is retroactive, we will amend the prior tax returns to file a claim for immediate expensing at such time.

Proposed Amendments to Bill C-208 – Tax Changes for Intergeneration Share Transfers

As noted in our July 29, 2021 tax alert, amendments to Bill C-208 are expected to be released soon. Any amendments to Bill C-208 will apply as of the later of November 1, 2021 and the date of publication of the final draft legislation. As we have yet to receive draft legislation, Bill C-208 and its more flexible conditions is still law. No draft legislation or update was provided with the economic statement.

We will continue to monitor these and provide relevant updates to clients via email and social media.

New Compilation Engagement Report

Replacing Notice to Reader standards

Those that manage a business and engage an accountant to prepare financial statements under what you may have previously referred to as a “Notice to Reader” engagement will have increased consultations, acknowledgement of your responsibilities and a new report attached. These strengthened requirements are due to the new Canadian Standard on Related Services (CSRS) 4200 Compilation Engagements, which is beginning for year ends ending on or after December 14, 2021.

What Changes Can You Expect in a Compilation Engagement?

The changes you can expect in a compilation engagement under this new standard can be outlined as follows:

- Your Accountant will ask you whether the compiled financial information is intended to be used by a third party (e.g., your lender) and whether the third party is in a position to request and obtain further information from you, and has agreed with you on the basis of accounting, before we accept or continue this engagement.

- A discussion about the expected basis of accounting (e.g. cash accounting with components on an accrual basis). Your accountant may help you select the basis of accounting; however, the basis of accounting is still your responsibility, and you will be asked to acknowledge this responsibility. The description of the basis of accounting will also be included in your compiled financial information.

- A new engagement letter that will include the objective and scope of the compilation engagement, the intended use of the financial information, the responsibilities of the practitioner, as well as your responsibilities and acknowledgments as specified in the new standard.

- A discussion of your business operations and accounting system to ensure we are performing the engagement in accordance with the new standard.

- A discussion about significant judgments that your Accountant has assisted management within the preparation of the compiled financial information (e.g. allowance for doubtful accounts) so that management understands their impact on the compiled financial information and accepts responsibility for them.

- Your Accountant may need to ask additional questions if they believe the compiled financial information appears misleading.

- You will acknowledge that you take responsibility for the final version of the financial information.

A new report will be attached to your compiled financial information that more clearly describes your responsibilities as management, the responsibilities of the Accountant and an explanation of the limitations of a compilation engagement.

As a result of the increased consultation and documentation, it is likely that the time required and fees will increase.

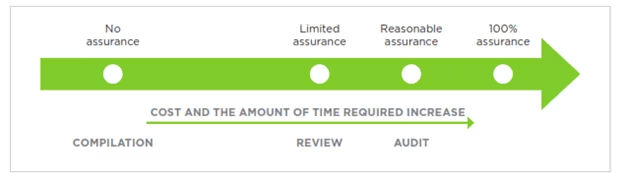

Is There Assurance Provided in a Compilation Engagement?

A Compilation Engagement under the new standard does not provide any form of assurance on the compiled financial information. To understand the scope, it is useful to illustrate the nature of various engagements as outlined in the following diagram:

When determining the type of engagement required for your organization or company, your Accountant can discuss differences between each type of engagement.

Ontario’s Not-for-Profit Corporations Act, 2010

The Ontario government has announced that the Not-for-Profit Corporations Act (ONCA), which provides a modern legislative framework for Ontario’s not-for-profit corporations (which includes registered charities that are incorporated), came into force as of October 19, 2021.

The ONCA generally applies to all Ontario corporations incorporated under an Act of the Ontario legislature that do not issue ownership shares, with limited exceptions.

The ONCA is intended to:

- simplify the incorporation process, making it easier and more efficient

- clarify rules for governing a corporation and increase accountability*

- clarify that not-for-profit corporations can earn a “profit” through commercial activities (e.g., selling T-shirts) as long as it is reinvested to support the corporation’s not-for-profit purposes

- allow some corporations to use a “review engagement” in place of an audit

- enhance members’ rights and outline actions they can take if they believe directors and officers are not acting in the corporation’s best interest

- give members greater access to financial records

Existing not-for-profit corporations will have a three-year transition period to make any necessary changes to their incorporating and other legal documents to bring them into conformity with ONCA. Any other requirements under the ONCA come into effect on October 18, 2021.

For full details on all governance and reporting requirements, see Ontario’s Guide to the Not-for-Profit Corporations Act, 2010 .

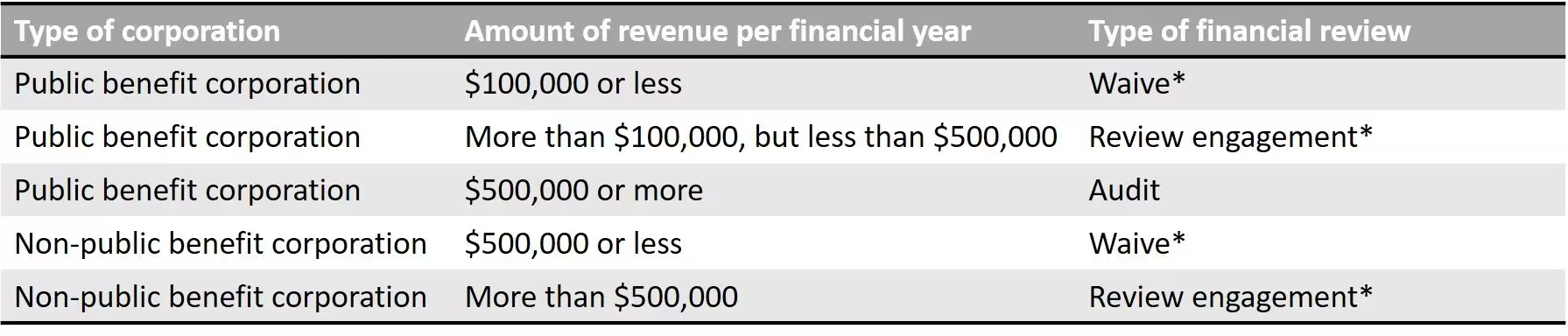

Accounting Engagements

The ONCA specifies thresholds for a compilation, review, or audit engagement to be performed on a corporation’s financial statements as follows:

* Approval to waive an audit or to waive both an audit and review engagement requires an extraordinary resolution , which is approval from at least 80% of the votes cast at a special members’ meeting where there are enough members to take a vote or if all voting members consent in writing.

There may be additional filing and reporting requirements under other statutes such as the Corporations Information Act and the Corporations Tax Act.

The Ontario government is expected to release more information regarding the ONCA.

Proposed New Trust Reporting Information Requirements

The Federal Government has proposed legislation that significantly expands trust reporting requirements. For taxation years ending on or after December 31, 2021, trusts that are required to file a T3 Trust Income Tax and Information Return will also be required to disclose the following information for each settlor, trustee, beneficiary and person who has the ability to exert influence over trustee decisions regarding appointment of income or capital of the trust:

- Name

- Address

- Date of Birth (in case of an individual)

- Jurisdiction of Residence

- Taxpayer identification number (Social insurance number, business number, etc.)

This new information schedule must be filed with the trust’s T3 return. It cannot be filed on its own.

For all existing clients, we have reviewed your situation and have reached out to you to get this information before the filing deadline of March 31, 2022. The deadline to return this information to us is December 31, 2021. If you have any questions about these new filing requirements or about the T3 return, please contact Becca Newbigging .

Regional Opportunity Investment Tax Credit (ROITC)

Canadian-controlled private corporations are now eligible to receive a 10-20% refundable tax credit if they purchase, construct or renovate a building (included in Class 1 or 6) over $50,000 and up to $500,000. The max credit available for additions in the periods below are:

- March 25, 2020 – March 24, 2021 – $45,000 tax credit

- March 25, 2021 – January 1, 2023 – $90,000 tax credit

This credit is available for each fiscal year in the qualifying period.

The building investment must be made in a designated region to qualify for the tax credit. The credit is issued based on the building location not the location of the corporations head office. Please note that any investment in Wellington County WILL NOT qualify for this tax credit as it is not in the designated region. A full listing of the designated regions are located on Ontario’s website .

If your company is a part of an associated group of companies, only ONE company in the group can claim the tax credit each year. The other companies in the associated group will need to elect in writing to waive their right to claim the ROITC.

Common Questions on the Principal Residence Exemption

How long do I need to live in a residence to claim it as a principal residence and qualify for PRE?

The CRA does not specify an exact duration of time an individual or their family members must reside in a dwelling for it to qualify as a principal residence for a given year. The tax rules refer to the residence being “ordinarily inhabited” within the calendar year. A more significant issue is whether a property held for a short period will produce an income gain (not eligible for the PRE) or a capital gain (usually eligible for the PRE) when sold.

The CRA will analyze evidence, such as length of time in the dwelling, sources of income and real estate buying patterns, to establish if the dwelling is indeed a principal residence or perhaps part of a business venture, such as real estate flipping.

If the CRA challenges your claim of exemption, they’re going to look at all the facts in the scenario. This could include looking into your intention of moving in and if something happen that forced you to sell.

Can other properties, such as a cottage, be designated a principal residence and eligible for PRE?

Most properties (home or cottage, for example) can be designated a principal residence – even those seasonal residences located outside of Canada, such as in the U.S. or Caribbean – as long as the owner or their family ordinarily inhabit it during each calendar year being claimed. Only one property per year, per family (spouse or common-law partner and children under 18), can be designated a principal residence.

Although it is becoming rare now, each spouse can designate a different property as a principal residence for years before 1982. Once sold, a property that isn’t deemed a principal residence will be subject to capital gains tax for the years it was not designated. A gain may also arise if the residence is designated for some, but not all, of the years of ownership.

There is also a restriction on land size that qualifies for the PRE. Property that exceeds one-half hectare (roughly 1.2 acres) will generally not qualify for the exemption. For example, if the property is a farm, only one-half of a hectare of land plus the home would qualify for the exemption, while the remaining acreage would be subject to capital gains tax based on value appreciation. If the excess land is required for the use and enjoyment of the property, then the land that qualifies can be larger. However, CRA is very restrictive when applying this rule.

When selling one of multiple properties owned, an owner can designate it as a principal residence for all or part of the years of ownership to take the best advantage of the exemption and minimize the amount of capital gains tax paid. Generally speaking, it makes sense to designate the property that has the highest average gain per year of ownership.

Can a property that generates income be deemed a principal residence and eligible for PRE?

The mandatory income tax reporting of a principal residence sale was introduced by the CRA to increase monitoring over foreign property ownership, “quick flips” or short holdings (on properties that may not qualify for principal residence status), properties that were not “ordinarily inhabited” every year by the owner, as well as serial builders who build and occupy a property before selling it.

Property that is used primarily to generate income or that is considered inventory does not qualify for PRE. This includes property that is solely rented out on a long- or short-term basis or one where the owner occupies one unit and rents out the others.

If an owner fails to report the selling of a principal residence, they could be subject to a late-filing penalty of $100 per month, up to a maximum of $8,000, according to the CRA. In addition, if an owner doesn’t report the sale on their tax return, the exemption may be denied and therefore the owner would be taxed on the capital gains.

If you have sold a property in the tax filing year, you should speak to your Accountant to assess how best to calculate and minimize your tax.

Bill 27 Working for Workers Act

On November 30, 2021 the Ontario legislature passed Bill 27. This bill amends various Ontario statutes. The two most significant changes are to the Employment Standards Act (ESA).

These changes are the right for employees to disconnect and limit on employers to include non-compete provisions in employment and other agreements.

- Right to disconnect: This amendment to the ESA affects any employer with greater than 25 employees. It will be effective in mid-2022. Employers will be required to have a written policy allowing employees to disconnect from work after hours. Disconnecting from work is defined as “not engaging in any work-related communications so as to be free from the performance of work”.

- L imit on use of non-compete provisions : This amendment to the ESA would prohibit any employer from entering into an agreement with an employee that includes a non-competition agreement. There are two exceptions when a business is sold and for an executive. This change to the ESA is effective October 25, 2021.

For more details on these two important changes to the ESA please contact [email protected] .

Hiring Virtually

- Prepare your questions: Be slightly more pointed in the way you ask questions. Some people are great at interviews and without in person cues, you may need to challenge them more. One solution could be to try questions that put the candidate into unique or challenging job-related scenarios. By taking the person away from a script, you can observe how they behave. If the response feels uncomfortable or evasive, dig in a little bit with follow-up questions.

- Connect creatively: Spend a few minutes getting to know the candidate and choose questions that showcase their personality, why they are interested in the role and organization. You need to listen very carefully, pay attention to facial expressions and tone, ensuring it comes across as comfortable.

Given that remote work is likely here to stay for many and that virtual hiring offers access to larger talent pools, we are likely to see more, rather than less, remote recruiting going forward.

Managing a Remote Workforce

Since the beginning of the pandemic, employers have been navigating the challenges of managing remote work. Virtual work, remote work, telework and work from home have now become the “norm” for many businesses. There are benefits and challenges to remote work for both employers and employees, as well as both Human Resources and Health and Safety considerations.

Challenges:

- Effective Communication

- Adequate Supervision

- Performance Management

- Technology needs and Information Security

- Employee Engagement and Collaboration

- Meeting Customer Needs

- Motivation and avoiding Distractions

Benefits:

- Reduced Overhead for the Employer

- Ability to weather the storm; business continuity in emergency situations

- Reduced Absenteeism when employees are sick, during inclement weather, etc.

- Increased size of the hiring pool with employees working from all over the province, country, and globe; more diverse workforce in terms of location, skills, experience, etc.

- Flexible hours for employees and better work/life balance to help with employee retention

- Reduced distractions from other workers

- Builds trust between the employer and employee and provides more autonomy to employees

The legal considerations for remote work are typically the same as the employer and employee obligations for work performed at the employer’s premises.

- Generally, all employee rights under the Employment Standards Act (ESA) still apply including wages, leaves, paid time off, etc.

- The Ontario Human Rights Code applies, especially in relation to accommodation and providing a workplace free from discrimination. Discrimination can take different forms including socioeconomic and family status relating to an employee’s ability to work from home.

- The Occupational Health and Safety Act may also apply to different remote work situations. The definition of workplace is broad and could include anywhere the employee performs work or acts in the course of employment. Therefore, the same general duties apply, as reasonable, to protect workers from hazards; such as ergonomic, electrical, fire, and harassment hazards.

- The Workplace Safety and Insurance Act applies to all duties performed in the course of and arising out of employment. This is determined based on the type of the activity and when and where it is performed; however, the tasks being performed is the primary factor. Injuries sustained that are related to work, while working remotely, may be covered by WSIB insurance.

When the pandemic started, employers rushed to arrange alternate arrangements for staff and may not have had time to consider all of the above factors or to prepare something in writing to clarify details of the remote working arrangements. Now that remote work has been ongoing and may have become permanent, having a written policy and agreement is an important step in managing remote employees. The policy should consider:

- What roles in the workplace are eligible for remote work?

- Will the arrangements be fully remote, hybrid, temporary, permanent…?

- What are the hours of work and the expected responsiveness to co-workers and customers?

- What technology is required and what will be supplied by the employer/employee?

- How will employees communicate with each other, with management, with customers?

- How will management oversee performance and what does success look like?

- What is the duration, time frame, right to recall the employees back to the workplace?

Employers should be clear in their expectations and employees are still required to meet those job expectations; however, flexibility and adaptability are key to successful remote work situations.

Your FIN (Financial Independence Number)

You only need two pieces of information to determine your Financial Independence Number:

- Your Basic Cost of Living

- Draw Down Rate

Your Basic Cost of Living is the total of your non-discretionary expenses annually. Things like housing, transportation, utilities, taxes, and healthcare to name a few. Your Draw Down Rate is the percentage of your assets you can utilize without reducing your capital. It is generally agreed upon that 4% is a reasonable and realistic Draw Down Rate for retirees.

Example

John and Jane want to know the amount of wealth that they must accumulate in order to retire comfortably based on their annual expenses of $60,000. They are comfortable with the rule-of-thumb Draw Down Rate of 4%.

Their Financial Independence Number (FIN) is easily calculated as:

FIN = Annual Expenses ÷ Draw Down Rate

= $60,000 ÷ 0.04

= $1,500,000

John and Jane’s Financial Independence Number is $1.5 Million, which is the amount of invested capital that they will need to fund their retirement and maintain their capital. Understanding this number will allow their financial advisor to assemble a plan to achieve this number, not just “earn as much as possible”.

The sooner you determine your Financial Independence Number, the sooner a plan to reach that goal can be built.

A Financial Planner can work with you to determine a savings budget and investment strategy to attain your retirement goals.

Spousal RRSPs To Reduce Taxes

Reducing Taxes Now and in Retirement

The contributor to an RRSP or a Spousal RRSP, receives the initial tax benefit. The contributor’s taxable income is reduced by the amount of the contribution. A $5,200 contribution ($100/week) reduces taxable income by $5,200 for the contributor whether it goes into their RRSP or into a Spousal RRSP.

While on-deposit, the investments are treated equally, growing tax free in an RRSP or a Spousal RRSP until the funds are withdrawn. (This assumes that the money is held in the Spousal RRSP for 3 years, otherwise any withdrawals are taxed as income for the contributor, not the spouse.)

At retirement, the household will rely on their savings in their RRSPs to generate income to cover their living expenses now that employment has ended. Both spouses in the couple would begin to withdraw from their RRSPs (or RRIFs). If there is a large discrepancy in the amounts in their RRSPs, one spouse could have a significantly higher income than the other when withdrawals are made during retirement.

All other things being equal, a couple with a high-income spouse and a low-income spouse will pay more income tax than a couple with equal levels of income. There are ways to split income between spouses, but they have limitations and are often under threat of being repealed.

As an example of the effects of balancing income without the aid of income splitting, a couple with one spouse earning $75,000 and the other at $0, will pay $11,881 in income tax in 2020. A couple with each partner earning $37,500 for a total of $75,000 will pay $9,792. A savings of more than $2,000 each year!!

As couples review their taxes each year, if spouses are in different brackets, they should consider using this strategy to lessen future taxes by having the higher income spouse contribute to a Spousal RRSP for the lower income spouse.

By the Numbers

Reminders

- Low-interest loans: The current family loan rate is 1%.

- Home buyers’ amount: Claim up to $5,000 of the purchase of a qualifying home, and get a non-refundable tax credit of up to $750.

Introducing Ward & Uptigrove Transactional Services

With a long term focus and over 20 years of experience, we have and continue to assist many of our clients in facilitating successful buy or sell. Our team of advisors surrounds you and can guide you through the transaction or even just provide a second opinion. We’ve established relationships with trusted business valuators, corporate commercial lawyers and lending relationship managers.

Our knowledge and reputation, along with our ability to assist in negotiating a fair deal, help the process go smoothly. Buying or selling a business should be a rewarding experience that is positive and memorable. Learn more about our Transactional Services web page or talk to your Accountant.

Ward & Uptigrove Donates to Help Offset Negative Impact of COVID-19

One Time Contributions to Selected Community Organizations

For over 60 years, Ward & Uptigrove has been a member of and given back to the community. Many charitable and community organizations have struggled to hold fundraisers and networking events this year.

In 2021, the Partners of Ward & Uptigrove selected charitable organizations for a one time, large donation. Partners have personal connections to these charities that play an active role in helping to make our community a great place to work and live. Many of these organizations have connections to our staff, clients or our community.

Supporting organizations that improve our community

- Listowel Memorial Hospital Foundation $40,000 in support of their ongoing contribution towards ensuring our community has first class medical facilities.

- Atwood Lions $4,600 in support of their ongoing contribution to local individuals, community groups and initiatives, such as the Atwood Lions full-sized outdoor ice rink.

Supporting organizations that help people, many with increased needs due to the COVID-19 pandemic

Ward & Uptigrove continues to also support many other organizations. Our contribution is a demonstration of our gratitude for some of the many great organizations that support individuals and our community.

Carbon Footprint Initiative

Ward & Uptigrove has joined the Carbon Footprint Initiative to champion Maitland Conversation’s goal of reducing the local carbon footprint and helping to improve the health and resiliency of the watershed to deal with the growing effects of climate change.

We’ve created a sustainability committee that has raised awareness with our staff and assisted with programs to reduce our carbon emissions including

- Transitioning office lighting to LED

- Remote working

- Transitioning to paperless

- Reducing waste, encouraging garbage free lunches

In 2022, we plan to further our commitment by investing in nature planting natural vegetation that sequesters carbon, clean up projects and fundraising initiatives.

Through the Maitland Conservation Foundation, individuals and businesses can contribute to projects that protect and enhance watershed forests, rivers and soil. To learn more, visit their website .

Staff Updates

As we reflect on 2021, our 63rd year, we recognize another year of growth and progression with our staff.

We are proud to congratulate the following staff members on their development and progression into new roles this coming year.

Partner & Principal Announcements

Michelle Vanderwal, CPA, CA

Partner

Jenny MacDonald, CPA

Principal

Agriculture Department Progressions

Vanessa Martin

Senior Accountant

Scott Stephenson

Senior Accountant

Maralee Parkhouse

Accounting Supervisor

Jill VanderWier

Senior Accountant

Chris Raben

Staff Accountant

Business Department Progressions

Amina Sulemanovski

Staff Accountant

Bookkeeping Department Progressions

Dianne Nonkes

Bookkeeping Team Lead

Cheryl Laffin

Senior Bookkeeper

Human Resources Solutions Progressions

Jennifer Goertzen

Senior H&S Professional

Emily MacRobbie

Senior HR Professional

Congratulations on your retirement!

Paul Hak, CPA, CMA

Partner

After 35 years with Ward & Uptigrove, Paul Hak is retiring from the Partnership and the firm. We are thankful for all of Paul’s contributions to the firm and wish him all the best in his retirement!

Welcome!

We are thrilled to welcome the following new staff members to our team:

Drew Chalkley

Accounting Support Consultant

Leah Frizzle

HR Professional

Deanna Furnemont

Payroll Administrator & Bookkeeper

Janelle Hill

Bookkeeper & Payroll Administrator

Virginia King

Bookkeeper

Bradyen Pellett

Staff Accountant

Luuk Postuma

Applications Analyst

Alexis Rock

Administrative Assistant

Kate Smith

Staff Accountant

Kristy Smith

Administrative Assistant, Wealth Management

Mark Tasker

Staff Accountant

Cassandra Watson

Staff Accountant